Incorporation of adjustments to the levelised cost for degradation are addressed on this page. A lot of assets degrade in different ways as do humans. In some cases like solar and batteries, the entire plant degrades meaning the output of the asset declines with age (this is happening to my brain and my declining output of excel models). With output degradation you can adjust the recovery and the operating expense to increase the cost per unit to cover the declining output. In other cases such as for hydrogen, the degradation applies only to an input item — maybe you need to eat more to maintain the same amount of work (this does not happen, you just get fat). For hydrogen you need to get more electricity. On this page I show you how to apply both types of degradation. I emphasize again that the you should worry much more about getting the levelised cost number right and less about your financial model which just proves that the levelised cost numbers are correct. The effects of degradation on levelised cost can include degradation only in input or fuel expense. The LCOE calculator attached to the button below can be used to evaluate degradation in the entire project or only the operating expense. Formulas and technical details are explained below.

.

.

Summary of Degradation Formulas

.

There is degradation of the total output which requires a kind of reverse inflation. The degradation calculations can be painful because they are different if you are using real or nominal LCOE and they require adjustments to both the capital charge portion of the LCOE and the operation and maintenance part of the LCOE formula. In general you can think of degradation as the opposite of inflation where things are getting smaller instead of getting larger (for inflation you can make adjustments for O&M expenses increasing and the overall price increasing).

Here is the step by step approach. Note that there are different degradation calculations for nominal LCOE and Real LCOE. When you make adjustments to the rates for PMT and for PV calculations, you should be careful with the denominator. Note that the tax adjustment — divided by (1-t) is made to the PMT function using the nominal IRR adjusted for degradation.

.

Part 1: Adjustments to Real LCOE for Overall Output Degradation.

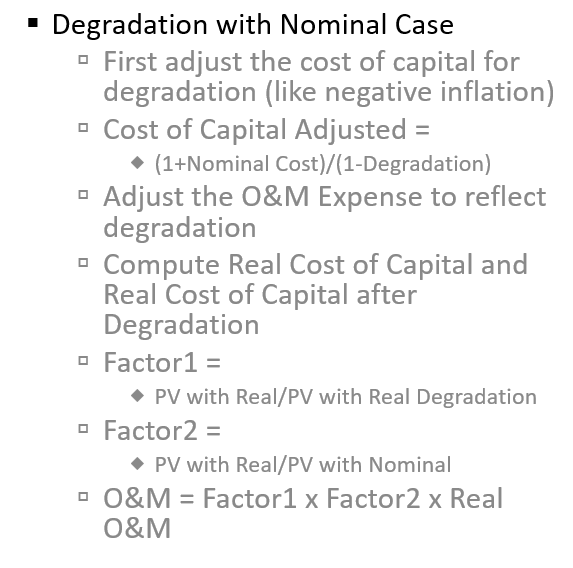

The first step with output degradation is to increase the capital charge rate to cover the gradual change in output with moves on a compound basis. As cost of capital reflects compound growth rate, you can adjust the degradation rate. When you make the denominator smaller, the cost increases.

Step 1: Compute Real Rate as (1-Nominal Rate)/(1+Inflation Rate) – 1

Step 2: Compute Real Rate with overall degradation effect:

Real rate with degradation = (1+real rate)/(1-degradation) – 1

This adjusted rate is applied to the PMT function and to the O&M function for overall degradation.

Step 3: Factor for O&M to increase O&M (Real rate with adjustment is higher):

When making adjustments for O&M expense, you can use the PV formula. The PV is bigger if the

Factor for Real O&M = PV(Real Rate Adjusted for degradation, Life,-1)/PV(Real Rate,Life,-1)

Real O&M = Initial Real O&M x Factor Above

.

Part 2: Adjustments to Nominal LCOE for Overall Output Degradation as with Solar Project

This section addresses the adjustment for degradation in LCOE computed on a nominal basis (I strongly belive the number for real LCOE is better). To do this start with the case of computing the carrying charge for the case where nominal levelized cost is computed — PMT(nominal rate, life, – initial cost). To include degradation, the PMT formula should be adjusted in a similar manner as it is in the real case for inflation. You can conisder degradation as negative inflation. If degradation occurs, then you must recover more money in nominal terms that accounts for the reduction in output over time.

In terms of the O&M adjustment for degradation in the nominal case, the calculation is a bit more confusing for me. The O&M goes up because O&M should inflate and the O&M goes up further because of degradation. So there are two adjustments to the O&M for nominal levelization. You compute a PV factor adjustment and use the real rate in the numerator and the nominal rate adjusted for degradation in the denominator. To begin the discussion, recall the inflation rate adjustment for O&M in the nominal case.

On another page I have explained how to make adjustments for inflation in operation and maintenance when computing the levelized cost on a nominal basis. The adjustment is necessary because the reported operating and maintenance is generally stated in current dollars or euros etc. — on a real basis. If you are computing the nominal LCOE and you have the real O&M expense, then you can increase the O&M Expense using the PV (not the NPV) formula in excel. You can think about the basic fact that if you use the PV formula with the life of the project, then the PV gives you a higher number when you have a lower discount rate.

Step 1: Compute the adjusted nominal IRR for degradation as

Adjusted Nominal Rate = (1+Nominal Rate)/(1-Degradation Rate) – 1

Step 2: Apply the Adjusted Nominal Rate in the PMT function

Step 3: Adjust the Initial O&M.

You can use a factor as follows:

Nominal Case: Factor = PV(Real Rate, Life, -1)/PV(Nominal Rate, Life, -1)

This factor will be above 1.0 if the inflation rate is positive and the real rate is below the nominal rate.

Now to the degradation adjustment. To begin, you can compute the real O&M cost using the PV formula. You can do this in two steps.

Adjustment Factor1 = PV(Real Rate, life, O&M)/PV(Degradation Adjused Real Rate, Life, O&M).

Adjustment Factor2 = PV(Real Rate, life, Adjusted O&M)/PV(Nominal, Life, O&M).

O&M for Nominal = Current O&M x Adjustment Factor2

.

Degradation with for a Single Expense Rather than the Entire Project (Hydrogen Case)

As stated above, for an electrolyzer the degradation can be for the quantity of electricity purchased rather than for the entire project. In this case you can adjust the single expense in an upward manner to reflect the increase in quantity required and apply the adjustment to the single (e.g. energy cost) expense. We begin by working with real data where there is no adjustment to O&M expense that increases the amount for inflation. In the first case we show the adjustment to real expense which isolates on the effect of the fuel expense degradation.

Step by Step Process for Adjustment to Real Expenses

Step 1: Compute the Real Discount Rate: (1+Nominal Target IRR)/(1+Inflation Rate) – 1

Step 2: Compute Real Rate Adjusted for Degradation : (1+Real Rate)/(1-Degradation Rate) – 1

Step 3: When things increase with a factor, put the lower discount rate at the bottom:

Factor = PV(Higher Degradation Rate in Step 2, Life, -1)/PV(Real Rate from Step 1, Life, -1)

Step 4: Adjusted Fuel Expense = Real Expense x Factor

.

Step by Step Process for Adjustment to Nominal Expenses

.

Adjusted Real = (1+Nominal)/(1-Real) – 1

Adjusted for Degradation = (1+Real)/(1+Degradation) – 1

Final Factor = PV(Real,Life,-1)/PV(Adjusted for Degradation,Life,-1)

.

.

.

.

Inclusion of Degradation in the Levelised Cost using adjustments to both Carrying Charges and O&M Costs

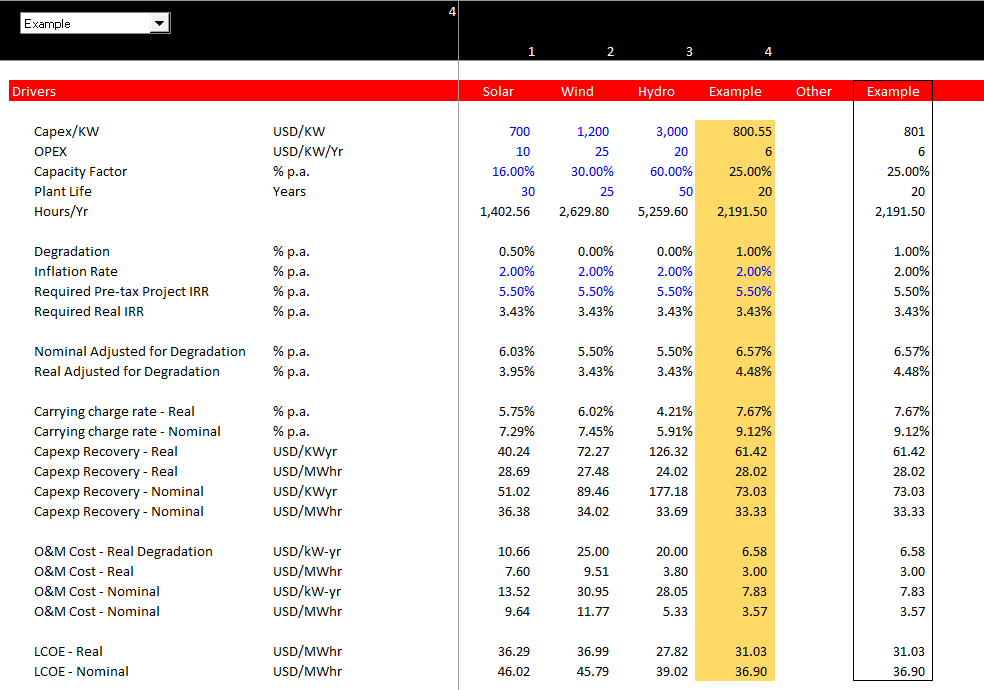

The formulas below evaluate levelised cost when the quantity of the units change. Different amount of units affects the weighting of the levelised price. For example, if the number of units is half of the units when the units start and if the price changes, then weighted average price changes. Without discounting, the screenshot below is 13.33. The price is not the average of 15.00 because you should give less weight to the price when there is less generation.

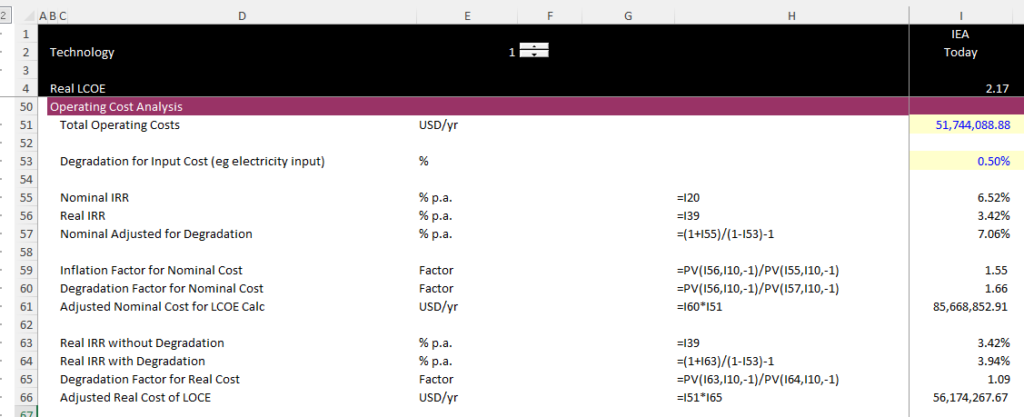

You should make changes to both nominal and real LCOE and you should make operating expense adjustments. The adjustments are represented by the following equations:

Adjusted Target IRR for Degradation = (1+Nominal IRR)/(1-Degradation)

Adjusted Real IRR for Degradation = (1+Real IRR)/(1-Degradation)

O&M Factor Nominal = PV(Real IRR,Life,-1)/PV(Adjusted Nominal IRR,life,-1)

O&M Factor Real = PV(Adjusted Real IRR,Life,-1)/PV(Real IRR,life,-1)

When you think about things, the levelised nominal cost is a silly number. Think about a hydro plant than may last 80 years. The nominal levelised cost is the flat value over 80 (with a minor adjustment for inflation in O&M expenses discussed below). With even a minor rate of inflation like 2%, the real value in 80 years is a very small percent of the value in the first year (divide by 1.02^80) — 4.9 times. It would be much better to compute the current value that, when inflated, gives you the target return. In simple terms this involves using a real cost of capital as described below.