This page will demonstrate different ways to compute to implied probability of default from credit spreads. Rather than having vague discussions of credit spread levels, the analysis begins with a base level of debt. Once a base debt issue like a risk free security is evaluated as a benchmark, the risk security is presented. Then, an analysis which uses expected value or risk neutral valuation is used to derive the implied probability of default. A file that illustrates how to compute the implied credit spreads is available for download below.

[wonderplugin_video iframe=”https://www.youtube.com/watch?v=YCfG5pUW4H8&t=3s” videowidth=600 videoheight=400 keepaspectratio=1 videocss=”position:relative;display:block;background-color:#000;overflow:hidden;max-width:100%;margin:0 auto;” playbutton=”https://edbodmer.com/wp-content/plugins/wonderplugin-video-embed/engine/playvideo-64-64-0.png”]

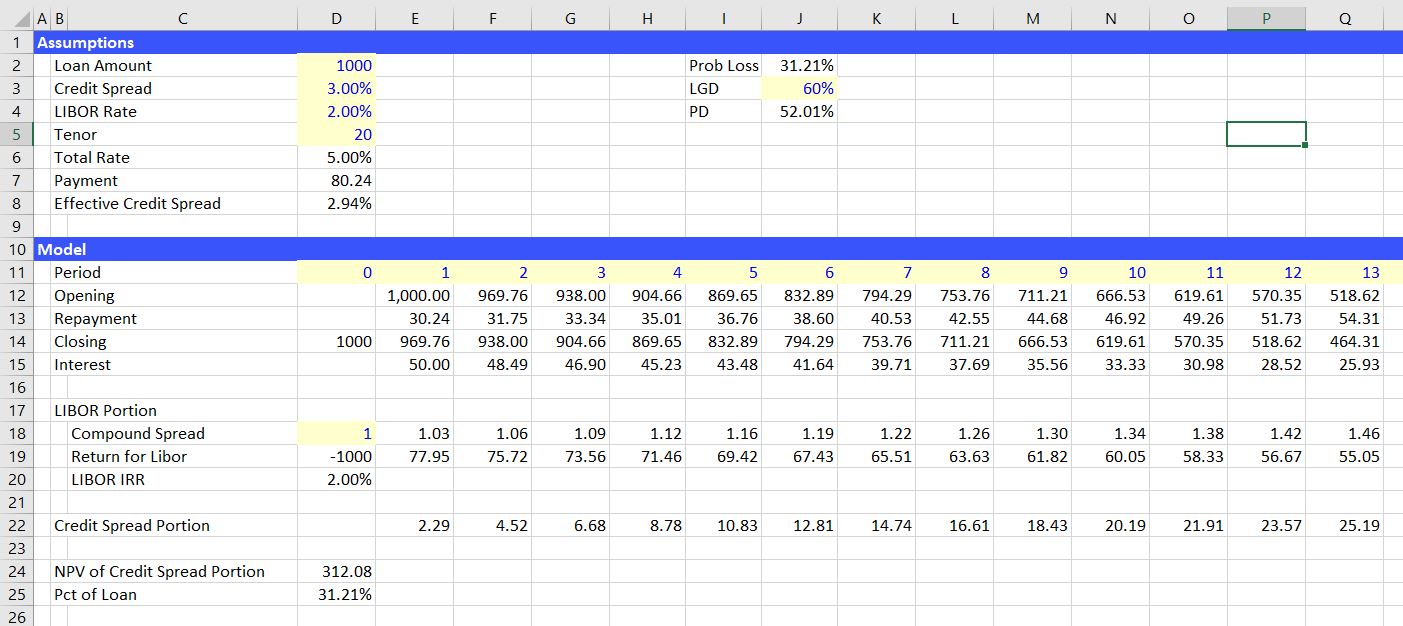

Implied PD from Credit Spreads

[wonderplugin_video iframe=”https://www.youtube.com/watch?v=MFXiAWzUxb4″ videowidth=600 videoheight=400 keepaspectratio=1 videocss=”position:relative;display:block;background-color:#000;overflow:hidden;max-width:100%;margin:0 auto;” playbutton=”https://edbodmer.com/wp-content/plugins/wonderplugin-video-embed/engine/playvideo-64-64-0.png”]

[wonderplugin_video iframe=”https://www.youtube.com/watch?v=CzqyIhUvg2A&t=136s” videowidth=600 videoheight=400 keepaspectratio=1 videocss=”position:relative;display:block;background-color:#000;overflow:hidden;max-width:100%;margin:0 auto;” playbutton=”https://edbodmer.com/wp-content/plugins/wonderplugin-video-embed/engine/playvideo-64-64-0.png”]

[wonderplugin_video iframe=”https://www.youtube.com/watch?v=cbFwhudakv8&t=346s” videowidth=600 videoheight=400 keepaspectratio=1 videocss=”position:relative;display:block;background-color:#000;overflow:hidden;max-width:100%;margin:0 auto;” playbutton=”https://edbodmer.com/wp-content/plugins/wonderplugin-video-embed/engine/playvideo-64-64-0.png”]